March marked, in our view, a shift in how markets are interpreting risk.

Geopolitical developments in the Middle East moved from a background concern to a primary driver behind stock and bond pricing, largely through their impact on energy, inflation, and the path of monetary policy.

As these pressures worked through markets, their effects became increasingly visible, contributing to challenging performance across both fixed income and equities. More importantly, it reflects a change in market behavior: investors are responding not just to events themselves, but to how those events might reshape what comes next.

In this environment, a couple of questions become particularly relevant:

- What is being priced into markets today?

- How should portfolios be positioned when outcomes remain uncertain?

The sections that follow address each in turn.

Monthly Market Recap

Fixed Income Markets

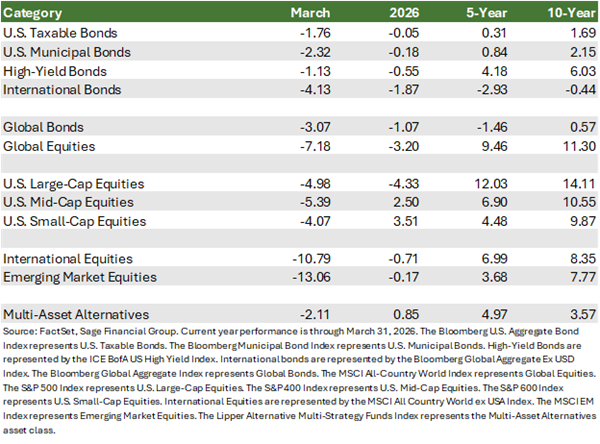

Bond markets faced a more challenging environment in March as rising energy prices and geopolitical uncertainty pushed inflation expectations higher, placing upward pressure on yields and exerting downward pressure on prices.

- U.S. taxable bonds declined 1.8% as persistent price pressures reduced expectations for Federal Reserve rate cuts this year. Higher rate expectations led to lower bond prices in March, and the asset class is down 0.1% in 2026.

- Tax-exempt bonds fell 2.3%, underperforming their taxable peers due to heavy market supply, which has been a key theme for 2026. Overall, performance is down 0.2% on the year.

- High-yield bonds retreated by 1.1% as widening credit spreads for much of the month reflected increased concern about default risk in sectors sensitive to AI disruption, such as software. Below-investment-grade bonds have experienced some pressure this year, declining 0.6% year-to-date.

- International bonds delivered a sharply negative return of 4.1%, pressured by higher global energy prices and by rates, which hurt import-sensitive economies like Europe and the UK. A sharp rebound in the U.S. dollar’s strength has pushed 2026 returns lower by 1.9%.

Fixed income did not provide the same degree of immediate diversification as in prior volatile periods, highlighting a more complex relationship between stocks and bonds when inflation concerns are at the forefront.

Equity Markets

Global equities declined throughout the month, with markets more closely intertwined with the conflict experiencing the largest declines.

- U.S. large-cap equities declined 5.0%, as geopolitical escalation in the Middle East raised uncertainty among investors concerned about sticky inflation and slower economic growth. Following this decline, large-cap stocks are down 4.3% year-to-date.

- U.S. mid- and small-cap equities declined 5.4% and 4.1%, respectively, reflecting similar concerns of higher rates, sticky inflation, and limited economic growth. Smaller stocks are more correlated with the Federal Reserve’s ability to cut the policy rate than large caps, a relationship that is becoming increasingly limited as the conflict persists. However, performance fared better as less revenue is derived internationally than from large caps. For the year, U.S. mid- and small-cap stocks are the strongest-performing segments, up 2.5% and 3.5%, respectively.

- International large-cap equities fell 10.8%, entering correction territory primarily driven by their high sensitivity to energy imports and the strengthening U.S. dollar, which eroded returns. Emerging market equities fared the worst, and lost 13.1%, as energy-dependent economies faced much steeper losses, whereas those with domestic fuel security in South America fared better. Despite the double-digit monthly decline, international large-cap and emerging-market stocks are down 0.7% and 0.2% in 2026, respectively.

Fixed Income: A More Complex Form of Diversification

Markets are currently pricing in a complex interplay between growth, inflation, and policy, largely driven by unrest in the Middle East. While geopolitical shocks have historically triggered a “flight to quality” that lowers yields, the current environment is less predictable.

Rising energy costs are a key reason. Higher oil prices have bolstered inflation expectations, limiting the traditional appeal of bonds even as uncertainty rises.

This creates a fundamental tension: the same forces dampening global growth are also inflationary. Consequently, central banks may find themselves constrained, unable to cut interest rates to support growth, even if economic conditions soften, until price pressures recede.

We expect the U.S. Federal Reserve to view these shocks as grounds to pause its current easing cycle, though we anticipate a resumption of rate cuts within the next 12 months. Conversely, the European Central Bank and Bank of England appear more inclined to hike rates to contain persistent price pressures.

This divergence in policy paths is beginning to shape how fixed income behaves across regions. It is no longer a uniform diversifier. Instead, returns are experiencing significant dispersion based on the dynamics of regional inflation and varying policy responses. This shift does not diminish the role of bonds; it refines it, requiring a more dynamic and selective approach than in previous cycles.

- High-quality bonds: Remain essential for income and stability. For example, in Q1 2025, high-quality fixed income returned 2.8% despite concerns about tariff-related growth. This role remains vital as markets balance inflation risks against potential economic weakness.

- Global Bonds: These offer valuable exposure as U.S. policy (pausing) diverges from Europe and Japan (hiking).

- Short-Duration High Yield: These provide high current income with lower sensitivity to interest rate fluctuations.

- Real Estate: As a portfolio complement, real estate serves as a physical asset hedge. Property values and rental income, particularly in non-cyclical sectors such as pre-leased data centers and student housing, often exhibit low correlation with fixed income and can adjust to keep pace with changing economic conditions.

Equity Markets: Multiple Pressures, not a Single Narrative

The same forces shaping fixed income, rising energy prices, shifting inflation expectations, and a more constrained Fed policy backdrop are also driving changes in global equity markets.

- International stocks: Disruptions to major shipping routes and oil infrastructure have added a geopolitical premium to commodity prices, raising costs for businesses and consumers globally and weighing especially heavily on international markets that depend on imported energy.

- U.S. stocks: The outlook is more mixed, with small-cap companies pressured by higher input costs and higher borrowing rates that are weighing on consumer activity. While large-cap technology stocks have at times served as relative stabilizers during volatile periods, current investor concern over the enormous AI infrastructure capex required has weakened demand.

More broadly, the market’s view of AI is shifting from rewarding potential to demanding durable earnings, contributing to greater dispersion and a more selective investment environment.

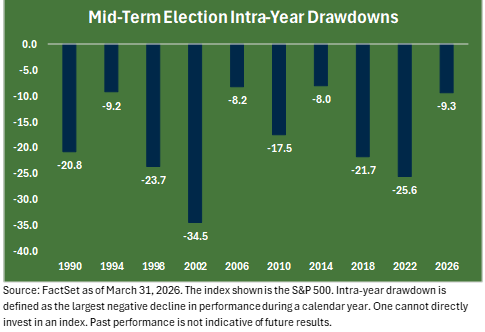

While this year’s 9.3% drawdown in U.S. large-cap equities may feel unsettling, such pullbacks are a typical hallmark of mid-term election years, which have seen the S&P 500 average a significantly deeper decline of 17.8% over the last ten cycles.

The resilience of the market is well documented by the 2022 downturn, in which indices fell 25.6% by October of that year. Since then, U.S. large-cap stocks have staged a robust 20.6% rebound per year return through March of this year.

From a positioning perspective, we believe this downturn at the start of the year presents both risks and opportunities. For example, global listed infrastructure is positioned to benefit from sustained fiscal spending and inflation-linked revenues and held up better in March than most international indices.

U.S. small-cap equities remain tied to domestic policy and consumer conditions, which remain supported by expansive fiscal policies enacted last year. International equities could participate more meaningfully in a recovery if the conflict ends and corporate profitability remains strong.

Closing Thoughts

March reflects an ongoing market transition from one defined by concentrated equity-market leadership and stable assumptions to one characterized by dispersion, repricing, and greater selectivity.\

Portfolio positioning in the current environment is less about predicting a single outcome and more about preparing for multiple paths forward. While geopolitical developments may continue to drive near-term volatility, we believe the longer-term drivers of returns, economic growth, and innovation remain intact.

Our focus remains on balancing opportunity and resilience, with investment decisions guided by our clients’ unique circumstances, goals, and time horizons, rather than short-term headlines.

Previous Posts

- Sage Insights: Market Observations Beyond the Tech Giants

- Sage Insights: Opening Bell: Observations from the Start of the Year

- Sage 2026 Investment Outlook: The Path to Resilience and Growth

- Sage Named Among Top Financial Advisory Firms

Learn More About Sage

Disclosures

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks, or estimates in this letter are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks, or assumptions should not be construed to be indicative of the actual events that will occur. These projections, market outlooks, or estimates are subject to change without notice. Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, product, or any non-investment-related content referred to directly or indirectly in this newsletter will be profitable, equal to any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer reflect current opinions or positions. All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual client portfolio returns may vary due to the timing of portfolio inception and/or client-imposed restrictions or guidelines. Actual client portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in managing an advisory account. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Sage Financial Group. To the extent that a reader has any questions regarding the applicability above to his/her situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. Sage Financial Group is neither a law firm nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of Sage Financial Group’s written disclosure statement discussing our advisory services and fees is available for review upon request. Copyright 2026.