One month into 2026, two forces continue to shape both the economic landscape and market behavior.

First, market leadership is broadening beyond a narrow group of U.S. companies, with international equities leading the way. This strength reflects a combination of earnings growth in select regions, expanding participation in the artificial intelligence cycle, and a weaker U.S. dollar that has benefited globally diversified investors. Second, artificial intelligence is moving from expectation to measurable impact as firms increasingly translate investment into productivity gains, margin support, and tangible earnings contributions.

Together, these dynamics help explain why markets have remained constructive, why leadership is becoming less concentrated, and why diversification, paired with selectivity, remains especially important as the year begins.

In this edition of Insights, we examine these themes and their implications for diversified portfolios.

Monthly Market Wrap

Fixed Income Markets

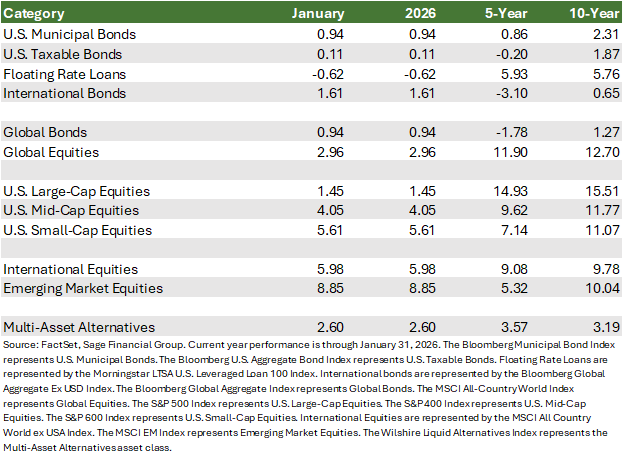

Fixed income markets began the year on a relatively stable footing as investors continued to assess the path of monetary policy amid moderating, but still positive, economic growth.

- U.S. taxable bonds posted modest gains of 0.1% as recent data reinforced expectations that the Federal Reserve is approaching the later stages of its easing cycle. In this environment, high-quality bonds continue to offer attractive income while once again serving as a meaningful source of diversification.

- Tax-exempt bonds benefited from steady demand and generally healthy credit fundamentals, gaining 0.9%.

- Floating-rate bank loans declined 0.6%, driven by elevated new supply and pressure on software names following disappointing earnings results.

- International bonds performed strongly, gaining 1.6% as the U.S. dollar continued to weaken, providing an additional tailwind for the asset class.

Taken together, fixed income has reestablished its role as both an income generator and a stabilizing force within diversified portfolios, something largely absent during much of the prior tightening cycle.

Equity Markets

In January, global equities continued to demonstrate broad resilience, with leadership rotating away from the tech-centric “Magnificent 7” of recent years toward a more balanced advance.

- U.S. large-cap equities posted a 1.5% advance, highlighted by the S&P 500 momentarily reaching the landmark 7,000 level. Yet results were mixed: semiconductor stocks climbed on AI-driven demand, while mega-cap software companies faced earnings pressure amid elevated spending.

- Mid- and small-cap stocks outpaced large caps, rising 4.1% and 5.6%, supported by a backdrop of moderating interest rates and domestic-oriented legislative support for cyclical stocks.

- International and emerging market (EM) equities have extended their streak of outperformance, rising 6.0% and 8.9%, respectively, propelled by a “perfect storm” of a weakening U.S. dollar and the broadening of AI trade globally.

Why International Equities Outperformed in January

International equities meaningfully outperformed U.S. markets in January, extending a trend that has been building beneath the surface. Importantly, this outperformance was not driven by a single global factor, but by a combination of region-specific fundamentals, sector leadership, and supportive currency dynamics.

In Europe, equity performance was supported by strong earnings growth in defense-related industries, as governments continued to increase military and security spending amid geopolitical realities. These commitments reflect longer-term fiscal priorities rather than short-term stimulus, providing a supportive earnings backdrop. At the same time, policy developments and budget discussions contributed to volatility, reinforcing the importance of selectivity within the region.

In Asia, the global artificial intelligence cycle continued to broaden beyond U.S. mega-cap technology firms. Companies in South Korea, Taiwan, and China, particularly those tied to semiconductors, advanced manufacturing, and AI-related hardware, benefited from rising demand linked to data-center buildouts and infrastructure investment.

In contrast to some U.S. technology leaders facing increased scrutiny around capital spending and return timelines, many of these firms are viewed as critical “picks-and-shovels” providers within the AI ecosystem and trade at more attractive valuations.

Currency movements also played a supporting role. Historically, periods of dollar softness have tended to coincide with stronger relative performance from international and emerging-market equities, though currency effects tend to amplify, rather than drive underlying fundamentals.

Taken together, recent performance highlights that tangible earnings growth, sector-specific catalysts, and a broader distribution of technological investment are driving international equity leadership. While performance has varied meaningfully across regions, the fundamental drivers supporting international markets remain in place.

For investors, this reinforces an important point: opportunities are not confined to any single geography. Maintaining global diversification, paired with selectivity within regions, is expected to position portfolios to participate in a wider range of growth drivers and reduce reliance on a narrow segment of the global market.

Artificial Intelligence: Productivity Is Becoming More Visible

Artificial intelligence remains one of the most important structural forces shaping the current market cycle. As we outlined in our Annual Outlook, AI is moving beyond early enthusiasm toward a phase where productivity gains are becoming more measurable and economically relevant.

At its core, AI is a productivity story. As companies integrate AI into both front-office and back-office functions, they are beginning to improve efficiency, reduce friction, and increase output without a proportional rise in costs. These gains can support margins even if revenue growth moderates.

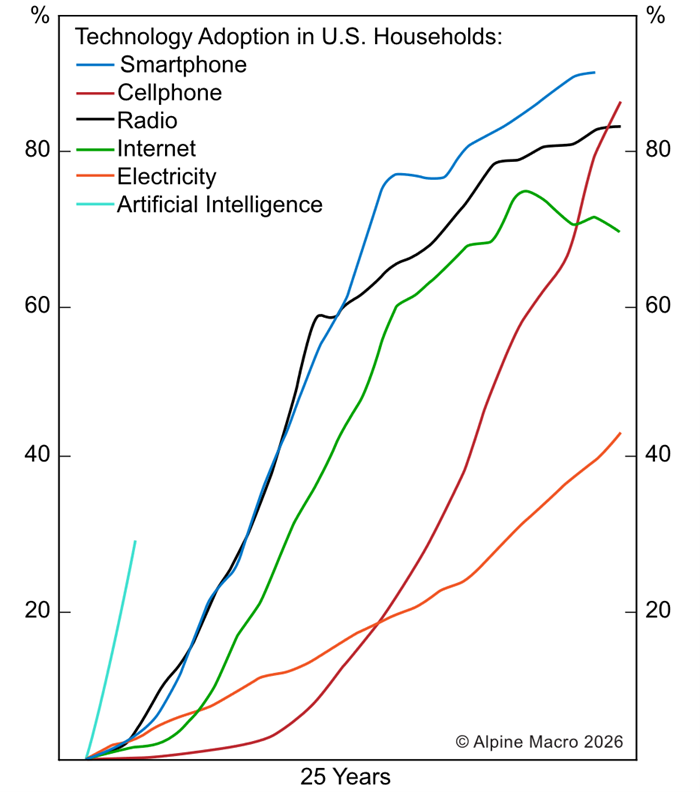

Notably, AI adoption has moved materially faster than many prior technological shifts, including the internet, electricity, and cellphones. The graphic below shows that uptake is occurring at about twice the rate of smartphones 20 years ago.

Over time, sustained productivity improvements can have broader macroeconomic effects.

- Lower Production Costs: Greater efficiency enables employees to produce more in the same time frame, helping contain unit labor costs.

- Increased Growth: When companies work more efficiently, their costs drop and profits rise. This prompts firms to reinvest in better technology and tools, creating a self-reinforcing cycle of economic expansion.

- Inflation Cools Off: As costs steady and supply increases, the overall upward pressure on prices begins to ease “at the margin”—meaning the most recent rounds of price gains start to taper.

If pricing pressures continue to moderate, central banks may gain greater flexibility even if growth remains resilient, allowing interest rates to drift lower without reigniting inflation concerns.

For fixed-income investors, we believe this productivity-driven disinflation supports the role of high-quality bonds as both income sources and portfolio stabilizers.

For equity investors, we believe it reinforces the importance of selectivity and discipline. While early AI-related market gains were highly concentrated, the next phase is likely to be more selective, both within and outside of the large-cap growth space. Companies that successfully translate technology into measurable efficiency gains may benefit regardless of whether they are viewed as traditional “AI leaders.”

Closing Thoughts

As 2026 progresses, markets appear to be in a period of transition rather than disruption. Market leadership is becoming less concentrated, global participation in key investment themes is expanding, and the economic impact of artificial intelligence is increasingly visible in corporate results.

In environments defined by dispersion rather than uniformity, discipline matters more than prediction. We seek to construct portfolios that increase the likelihood that clients achieve their financial objectives across a broad set of economic conditions and market environments. Maintaining diversification, staying selective, and remaining focused on financial objectives is often more effective than reacting to short-term narratives or narrow leadership trends.

At Sage, we continue to position portfolios to balance opportunity and resilience, aiming to keep our clients’ investments aligned with their goals, unique circumstances, and risk tolerance across a range of market environments.

Previous Posts

- Sage 2026 Investment Outlook: The Path to Resilience and Growth

- Sage Insights: Fed Policy Turning Point, AI Enters a New Phase

- Sage Named Among Top Financial Advisory Firms

Learn More About Sage

Disclosures

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks, or estimates in this letter are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks, or assumptions should not be construed to be indicative of the actual events that will occur. These projections, market outlooks, or estimates are subject to change without notice. Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, product, or any non-investment-related content referred to directly or indirectly in this newsletter will be profitable, equal to any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer reflect current opinions or positions. All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual client portfolio returns may vary due to the timing of portfolio inception and/or client-imposed restrictions or guidelines. Actual client portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in managing an advisory account. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Sage Financial Group. To the extent that a reader has any questions regarding the applicability above to his/her situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. Sage Financial Group is neither a law firm nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of Sage Financial Group’s written disclosure statement discussing our advisory services and fees is available for review upon request. Copyright 2026.