Executive Summary

As we enter 2026, we view markets as continuing to transition from a period defined by concentrated equity leadership and policy uncertainty toward a more balanced, potentially broader set of opportunities. 2025 delivered strong headline returns across global equities and fixed income, with returns of 22.3% and 8.2%, respectively. International equities outperformed U.S. equities, while bonds were a stabilizing component of portfolios. Moving forward, an important question for investors is how the forces shaping markets are evolving.

Our Outlook for 2026 is constructive, but disciplined.

We believe that three structural forces are likely to exert an outsized influence on returns in the year ahead.

1. Artificial intelligence remains a powerful driver of economic change. But the investment opportunity is likely to shift from early beneficiaries to infrastructure, applications, and companies that can benefit from broad productivity gains.

Early enthusiasm rewarded a narrow set of companies directly tied to AI infrastructure. As capital spending accelerates and valuations remain elevated in parts of the market, differentiation is increasing. We believe the next phase of AI-related opportunity and equity performance will be driven by tangible profitability and cash flow generation rather than AI-theme sentiment.

2. Monetary and fiscal policies act as economic tailwinds.

The Federal Reserve has shifted toward easing as growth moderates, while fiscal initiatives continue to support corporate investment and consumer spending. Historically, this combination has provided a constructive backdrop for debt, stocks, and alternatives alike.

3. Investor and consumer sentiment remains unusually subdued, which tends to be a positive sign for stock markets going forward.

Despite strong market performance, confidence remains low by historical standards. Periods of pessimism have often created opportunities for disciplined investors. Over the last 40 years, when market sentiment reaches a low point, as it is now, the average 12-month forward return on the S&P 500 has been 25.0%.

Taken together, these forces point to a year in which market leadership may continue to evolve, and diversification across asset classes and geographies becomes increasingly important.

From a portfolio perspective, our goal is to prepare for a variety of outcomes in economic growth and financial markets. This portfolio construction focuses on several core principles:

- Maintaining equity exposure across geography and style while managing valuation and concentration risk

- Combining high-quality bonds with higher-yield bonds to balance interest rate exposure and credit risk sensitivity

- Including commercial real estate and infrastructure to provide real-asset exposure that may perform well in economic environments different from those favoring traditional stocks and bonds

- Remaining disciplined through rebalancing rather than reacting to short-term volatility

While past performance does not indicate future results, we believe a diversified, selective, and balanced approach provides the most reliable foundation for navigating uncertainty. In our view, this disciplined strategy gives investors the highest probability of meeting their financial goals.

2025 In Context: Setting the Stage for a Changing Market Cycle

The defining feature of 2025 was not simply strong market performance, but the way that performance unfolded. The year began amid elevated policy uncertainty, with renewed trade tensions and proposed tax changes, including tariffs, weighing on investor sentiment and contributing to early market volatility.

As the year progressed, those concerns began to ease. Economic growth moderated, labor market conditions softened, and inflation continued its gradual descent, creating the conditions for a shift in monetary policy. After holding rates steady for much of the year, the Federal Reserve initiated a series of rate cuts in the second half of 2025.

Notably, these rate cuts occurred while the economy remained on a stable footing. Growth continued, credit conditions held firm, and financial stress remained contained. Historically, easing cycles that begin amid economic resilience, rather than a recession, have tended to support both equity and fixed-income markets.

At the same time, corporate earnings proved more resilient than many investors expected.

Companies tied to artificial intelligence and advanced technology continued to exceed expectations, helping propel U.S. equities to new highs. Elsewhere, improving policy clarity and a weaker U.S. dollar supported strong performance across international markets.

By year-end, both global bonds and global equities delivered solid returns. However, beneath the surface, important dynamics were taking shape: market leadership became increasingly concentrated, valuations expanded in select areas of the market, and interest rates began to normalize from restrictive levels.

These conditions shape the opportunity set entering 2026. Understanding how 2025 unfolded is essential not because it predicts what comes next, but in our view, because it explains why diversification, selectivity, and discipline are now more important than they were a year ago.

Fixed Income in 2025: Rate Cuts into Strength

Fixed income markets in 2025 were shaped primarily by the timing and direction of Federal Reserve policy. For much of the year, policymakers remained on hold as they assessed the combined effects of moderating economic growth, tariff-related uncertainty, and inflation above the Fed’s long-term target.

That stance shifted in the second half of the year. As labor market conditions softened, the Federal Reserve began easing policy, delivering rate cuts in September, October, and December. Notably, these cuts occurred while economic growth remained positive and credit conditions stayed relatively stable, an environment that proved supportive for bond markets.

As yields declined, investor demand shifted from cash to income-producing assets. For the full year, U.S. taxable bonds returned 7.3%, while tax-exempt bonds gained 4.3%, reflecting both income generation and modest price appreciation as rates moved lower.

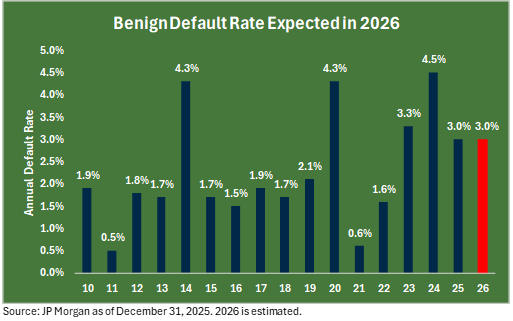

Floating-rate loans also performed well, returning 7.2% in 2025. Elevated short-term interest rates and generally healthy corporate fundamentals supported returns, while the senior-secured structure of these instruments helped limit downside during periods of volatility. Although the asset class experienced brief stress in October, default rates finished the year near the 25-year average of approximately 3.0%.

International bonds were another source of strength, returning 8.8% for the year. Attractive starting yields and an earlier, synchronized shift toward easier monetary policy across major global economies drove performance. A weaker U.S. dollar further enhanced returns for U.S.-based investors, underscoring the diversification benefits of global fixed income exposure.

By year-end, fixed income had reestablished its role as both an income generator and a stabilizing force within diversified portfolios, setting the stage for how we are now thinking about bond positioning heading into 2026.

Equities in 2025: Strength At Home, Positive Signals Abroad

Global equity markets rebounded sharply in 2025, overcoming tariff-related volatility early in the year to close near all-time highs. While returns were strong across regions, the defining feature of the year was how leadership unfolded.

U.S. Equities: Concentrated Leadership Played Out as Expected

Global equity markets delivered strong results in 2025, with broad gains across regions but uneven below the surface. While headline returns were impressive, the defining feature of the year was concentrated leadership, particularly within U.S. markets.

As a continuation of a multi-year trend, U.S. equity performance was driven primarily by a narrow group of large-cap technology and AI-focused companies. The S&P 500 posted a strong full-year gain, but much of that return was attributable to a small number of names.

Information technology and communication services together accounted for roughly two-thirds of the S&P 500’s total return in 2025. These sectors—home to companies such as Nvidia, Apple, Microsoft, Broadcom, Meta Platforms, and Alphabet—rose 24.0% and 33.6%, respectively, reflecting continued enthusiasm for AI-related investment and earnings growth.

Mid-cap and small-cap stocks lagged for much of the year, rising by approximately 7.5% and 6.0%, respectively. Higher financing costs and investor preference for perceived balance-sheet strength weighed on smaller companies early in the year. However, as financial conditions eased later in 2025, smaller-cap equities began to recover, a potential signal that market leadership may be broadening.

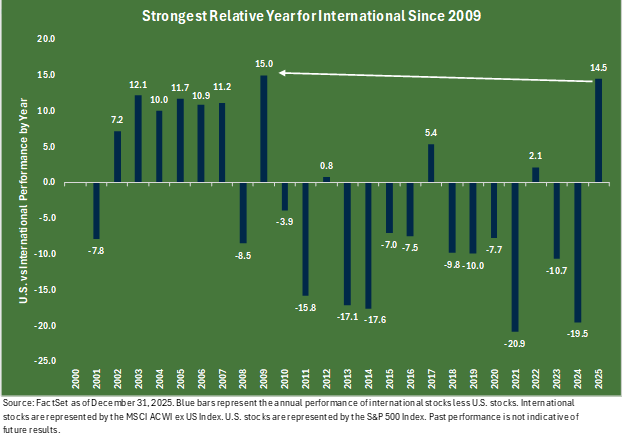

International Equities: Catch-Up Fueled by Valuation and Currency

International equities delivered particularly strong returns in 2025, gaining 32.4% for the year. A key driver was the sharp weakening of the U.S. dollar—down roughly 9.4% against major currencies—which amplified returns for U.S.-based investors.

The U.S. dollar declined as the Federal Reserve lowered interest rates, eroding the yield advantage that previously attracted global capital. This weakness was compounded by market volatility stemming from trade tariffs and growing concerns about fiscal sustainability, as the national debt exceeded $38 trillion.

Valuations also played an important role. Non-U.S. equities entered the year trading at meaningful discounts to U.S. markets, setting the stage for a valuation-driven “catch-up” rally as earnings growth remained resilient and policy uncertainty eased.

Emerging market equities were among the strongest performers, returning 33.6% in 2025. Performance was supported by a falling dollar, improving earnings expectations, attractive valuations, and continued investment in technology and manufacturing capacity across key regions.

Chinese stocks staged a rebound, with the MSCI China Index rising nearly 31.2%. This performance was driven by significant AI advancements and government policy support, including trillions in credit for stock repurchases and direct ETF purchases to stabilize the market.

What the Equity Experience in 2025 Reinforced

The equity experience of 2025 reinforced several core themes from last year’s Outlook: narrow leadership, elevated valuations in select segments, and wide dispersion across regions and market capitalizations. While headline returns were strong, these underlying dynamics shaped today’s opportunity set.

For investors, the lesson is not to extrapolate last year’s winners indefinitely, but to recognize how conditions are evolving. Concentration creates both opportunity and risk, and periods of shifting leadership have historically rewarded diversified exposure rather than narrow positioning.

Diversified Portfolios: Remaining Disciplined

Periods of market stress often test investor behavior more than economic fundamentals. In 2025, short-lived but sharp bouts of volatility challenged investor confidence, even as underlying economic conditions remained relatively stable.

Early in the year, renewed trade tensions and policy uncertainty triggered a sharp selloff from January 1 to April 2 (Tariff announcements/Liberation Day), briefly pushing major equity indices into bear-market territory and erasing trillions of dollars in market value. As we noted in last year’s Outlook, episodes like these tend to challenge investor conviction more than long-term fundamentals.

Diversified portfolios were designed to withstand these environments. Exposure across asset classes helped mitigate drawdowns, while maintaining market participation allowed portfolios to benefit as conditions improved. The recovery that followed was swift, underscoring the risk of exiting markets during periods of elevated uncertainty.

Fixed income played a stabilizing role as the year progressed, contributing income and diversification as yields declined later in the year. Equity exposure provided growth as markets recovered, while international diversification reduced reliance on any single region or outcome.

For investors, the central lesson of 2025 was not simply that markets rebounded, but that process mattered. A disciplined approach—grounded in diversification, periodic rebalancing, and alignment with long-term objectives—proved more effective than attempts to time markets or respond emotionally to headlines.

This lesson carries directly into 2026. While past performance does not indicate future results, the value of discipline remains constant. We continue to believe that diversified portfolios, tailored to each client’s goals and risk tolerance, provide the most reliable foundation for navigating uncertainty and pursuing long-term investment objectives.

Our 2026 Investment Outlook

The following table summarizes the key themes Sage identified in the 2025 outlook. For each, we share the commentary that informed our Outlook, an outcome-based grade, and a recap of the year’s events.

Key Themes For 2026: The Path to Resilience and Growth

Looking ahead to 2026, we believe three structural forces will exert an outsized influence on returns across asset classes. The conditions that shaped markets in recent years—concentrated equity leadership, elevated policy uncertainty, and unusually tight financial conditions—are beginning to evolve.

Rather than anchoring portfolios to a single forecast, our approach focuses on identifying the dominant economic and market forces most likely to shape opportunities and risks. These themes are not predictions; they are frameworks for navigating an environment where growth, policy, and sentiment are all in motion.

We believe three themes are particularly relevant as we enter 2026:

- Theme #1: Artificial intelligence is entering a more discerning phase, as markets shift from rewarding participation to demanding execution, efficiency, and durable earnings.

- Theme #2: Monetary and fiscal policy are increasingly aligned, creating a supportive—but not risk-free—backdrop for growth and asset prices.

- Theme #3: Investor and consumer sentiment remains unusually subdued, a condition that has historically rewarded disciplined investors willing to look beyond near-term uncertainty.

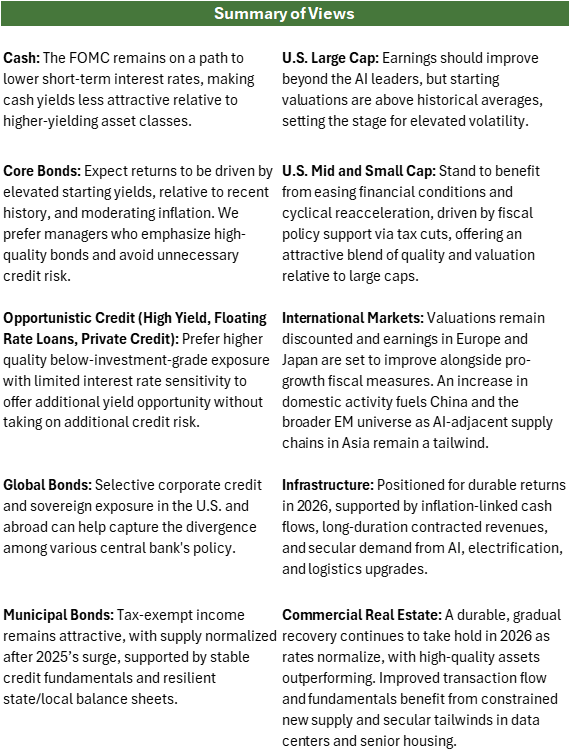

Below is a summary of our selective views by asset class for investments we currently recommend for most client portfolios. Other asset classes, including but not limited to commodities, emerging market debt, and cryptocurrency, are not being recommended for client investments at this time, unless specifically requested.

Together, these themes reinforce our emphasis on diversification, selectivity, and discipline. As we explore each in greater detail, our focus will be on understanding how these forces may shape risks and opportunities and how we can thoughtfully position portfolios in response.

Theme #1: Powerful AI, Premium Price

Artificial intelligence remains one of the most powerful economic forces reshaping the global economy. The rapid advancement of large language models and related technologies represents a structural shift with the potential to influence productivity, capital investment, and corporate strategy across a wide range of industries.

From an investment standpoint, however, the AI narrative is entering a more discerning phase. Early enthusiasm rewarded a narrow group of companies viewed as essential enablers of AI development. As capital spending has accelerated and valuations in parts of the market have expanded meaningfully, markets are increasingly demanding evidence of durable earnings, capital discipline, and returns on investment.

The Four Phases of AI Value Creation

We continue to view the AI opportunity as unfolding across four overlapping phases, each with distinct risks and return drivers.

Phase 1: Direct Beneficiaries

Chipmakers and equipment suppliers were the earliest beneficiaries of AI adoption, with revenues tied directly to model training and inference. We believe that much of this value creation has already been reflected in market prices, leaving valuations elevated and increasing sensitivity to earnings delivery.

Phase 2: Infrastructure Build-Out

The market is now firmly in this phase. Hyperscalers and cloud providers are investing aggressively to expand AI capacity, driving demand for data centers, power generation, cooling systems, and advanced networking. While this investment reflects confidence in long-term adoption, it also raises important questions about capital efficiency and returns as spending scales.

Phase 3: AI-Enabled Applications

We believe the next phase will be defined by companies that successfully monetize AI through software, services, and industry-specific applications. Outcomes here are likely to vary widely. Competitive advantage will depend on data quality, pricing power, and customers’ willingness to pay for incremental productivity gains.

Phase 4: Broad Productivity Gains

Over time, AI’s most durable impact may emerge through broad-based productivity improvements across the economy. Companies outside the technology sector may benefit from cost efficiencies, margin expansion, and improved decision-making—often without being labeled “AI companies” by the market. In 2026 alone, Amazon, Microsoft, and Google are each expected to spend more than $100 billion, totaling more than $300 billion among them.

Where Risks Are Emerging

While AI’s economic potential remains compelling, we believe the investment landscape is not without vulnerabilities. Four dynamics warrant careful attention:

- Capital intensity: Training and deploying advanced models require significant upfront investment, raising the hurdle to profitability and increasing barriers to entry.

- Circular financing: Venture and private funding continue to support innovation, but paths to durable, capital-efficient business models remain uncertain for many firms.

- Talent constraints: Severe talent and skills shortages in specialized AI roles continue to drive up the cost of maintaining expert teams.

- Regulatory and social pressure: There is a growing backlash against artificial intelligence, fueled by concerns over job displacement, privacy, and control, which is likely to generate political momentum for far more aggressive regulation.

As AI’s energy demands grow and its social footprint expands, these pressures may influence both costs and public policy in ways markets have not fully priced in.

What This Means for Investors in 2026

The AI opportunity is not disappearing, but it is changing. Markets are moving beyond rewarding companies simply for participating in the AI narrative and are increasingly differentiating on the basis of execution, efficiency, and valuation.

For equity investors, this argues for selective exposure across the AI ecosystem rather than concentrated positioning in a small group of market leaders. We favor a balanced approach that includes infrastructure, enabling services, and potential downstream beneficiaries—while remaining disciplined on price.

For fixed-income investors, AI-driven productivity gains may prove structurally disinflationary over time, reinforcing the role of income-oriented investments and portfolio diversification.

In short, AI remains a powerful driver of growth, but the next phase is likely to reward discipline over enthusiasm.

Theme #2: Twin Tailwinds – Policy Propels Markets

As we look ahead to 2026, the investment landscape is increasingly shaped by the combined influence of monetary and fiscal policy. Unlike recent years, when policy uncertainty often weighed on confidence, we believe the coming year is likely to be defined by two policy engines pushing in the same direction. In our view, this alignment represents one of the most constructive forces for markets entering 2026.

Monetary Policy: Easing with the Dual Mandate in Focus

Importantly, monetary policy support is emerging amid moderating growth rather than economic stress. Historically, easing cycles that begin in the context of economic resilience—rather than recession—have tended to extend market cycles rather than merely cushion downturns.

The Federal Reserve enters 2026 having already begun to ease. After holding rates steady for much of 2025, policymakers began cutting rates as labor market conditions softened, even as inflation remained above the Fed’s long-term target. This shift reflected growing concern that employment risks were beginning to outweigh lingering inflationary pressures.

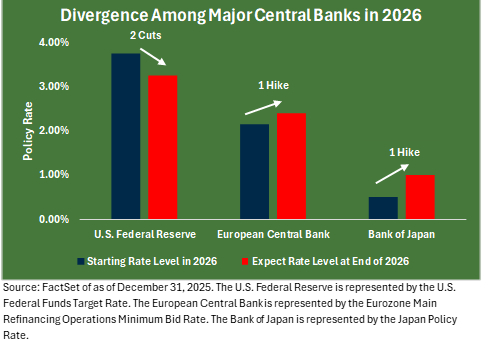

Outgoing Fed Chair Jerome Powell has described policy as “modestly restrictive,” leaving room for additional cuts should economic data weaken further. With Powell’s term set to expire in May, attention has turned to the policy stance of the incoming chair. Public comments from potential successors suggest continuity rather than reversal, reinforcing expectations for a gradual easing bias. Below is the forecast for 2026 rate cuts from FactSet Estimates. Forecasts can change quickly over a calendar year, as economic data surprises can deviate from market expectations.

For investors, this environment lowers borrowing costs and supports interest-sensitive areas of the economy. At the same time, it increases the importance of selectivity, as the pace and magnitude of rate cuts are likely to remain data-dependent rather than preordained.

Fiscal Policy: Sustained and Targeted Support

Alongside monetary easing, U.S. fiscal policy remains expansionary. Legislation aimed at restoring favorable tax treatment for capital investment, including full expensing provisions, is designed to improve corporate cash flow and incentivize business spending.

At the same time, large-scale initiatives such as the CHIPS and Science Act continue to support domestic manufacturing and technology investment. These programs remain central to the ongoing build-out of AI-related infrastructure and provide longer-term visibility for capital-intensive industries.

For markets, this combination of government spending and investment incentives helps create a baseline level of demand that can cushion periods of slower private-sector activity. For investors, it increases the likelihood that earnings growth will remain more resilient than headline economic growth alone suggests.

What the Policy Backdrop Means for Investors

When monetary and fiscal policy move in tandem, the resulting impulse has historically supported both corporate earnings and asset prices. Lower financing costs can support valuations, while fiscal spending helps sustain demand and investment.

That said, policy alignment does not eliminate risk. Inflation remains a key variable, and policy paths are rarely linear. For this reason, we view the current environment as constructive rather than complacent.

For equities, this backdrop supports the case for broader participation beyond a narrow group of leaders. For fixed income, it reinforces the role of income and carry as rates normalize, while underscoring the importance of managing duration and credit exposure thoughtfully.

Theme #3: When Sentiment Sours – Capitalizing on Crowd Psychology

Investor sentiment often reflects emotion more than fundamentals. As a result, it can provide helpful context for how markets are positioned—particularly at extremes. Entering 2026, consumer and investor sentiment measures remain near multi-year lows, despite a period of strong market performance and resilient economic conditions.

The University of Michigan Consumer Sentiment Index captures households’ views of their financial situation and economic prospects. Historically, the index has been volatile and reactive to inflation concerns, policy uncertainty, and headline risk. Over longer periods, however, sentiment has tended to function as a contrarian indicator rather than a forecasting tool.

Over the past three decades, forward 12-month equity returns following sentiment peaks have averaged approximately 4.3%, while returns following sentiment troughs have averaged closer to 25.0%. These figures do not suggest that sentiment predicts near-term market direction, but they do highlight how pessimism has often coincided with more attractive long-term entry points.

For investors, the implication is not to act on sentiment, but to recognize its influence. Periods of depressed confidence often coincide with increased volatility and emotionally driven decision-making. Attempting to time markets during these moments can be costly—particularly if it results in reducing exposure just as long-term opportunities improve.

This reinforces a broader principle as we move into 2026: successful investing often requires doing the opposite of what feels comfortable. Remaining committed to a disciplined, diversified strategy—rather than reacting to pessimistic narratives—has historically improved the likelihood of achieving long-term financial goals.

Positioning for 2026: From Themes to Portfolios

The themes shaping the investment environment in 2026—technological change, evolving policy dynamics, and subdued sentiment—do not point to a single outcome. Instead, they highlight the importance of thoughtful portfolio construction and asset-class selectivity.

Our asset-class views are informed by these forces and grounded in valuation, fundamentals, and risk compensation. While market leadership may continue to evolve, our focus remains on positioning portfolios to participate in opportunities while managing downside risk.

In the sections that follow, we outline our Outlook for major asset classes and explain how current conditions influence our approach to equities, fixed income, and other portfolio components. As always, these views are implemented within diversified portfolios tailored to each client’s objectives, risk tolerance, and time horizon.

Fixed Income Outlook: Navigating the Fed’s Dual Mandate

Entering 2026, fixed income markets sit at the intersection of moderating growth and persistent inflation uncertainty. The Federal Reserve continues to balance its dual mandate—supporting employment while keeping inflation under control—leaving limited room for policy missteps.

While inflation has cooled meaningfully from prior peaks, it remains above the Fed’s long-term target. At the same time, labor market conditions have softened, increasing pressure on policymakers to continue easing. This tension suggests that future rate decisions are likely to remain data-dependent and uneven, contributing to periodic volatility across interest rate markets.

For investors, this argues against a single, directional view of interest rates. Instead, flexibility, diversification, and income generation remain central to fixed income strategy in 2026.

Cash and Core Bonds: Locking in Income as Rates Normalize

As the Federal Reserve moves deeper into an easing cycle, yields on cash and money market instruments are likely to decline. In contrast, core investment-grade bonds continue to offer the opportunity to lock in income at yields that remain attractive by historical standards. Robust annuity sales remain a primary catalyst for investment-grade bond demand.

We maintain a neutral stance toward intermediate-duration, high-quality bonds. While price appreciation potential may be limited, these securities continue to play an important role in diversified portfolios—providing income, liquidity, and ballast during periods of equity market volatility.

Global Bonds: Opportunities Beyond the U.S.

Global fixed-income markets offer increasingly compelling opportunities as we enter 2026. After years of aggressive tightening, yields across developed international markets are now near their highest levels since before the global financial crisis. Below is the forecast for global policy rate expectations in 2026 from FactSet Estimates. Policy rates are targeted and adjusted by central banks to influence the cost of borrowing within economies.

As monetary policy paths diverge across regions, selectively adding global bond exposure can enhance diversification and income potential. Given persistent domestic risks—including inflation uncertainty and rising government debt—we believe global fixed income remains an important complement to U.S.-centric allocations.

Floating Rate Loans: Income with Structural Protection

Floating-rate loans continue to offer attractive income potential, supported by elevated base rates and generally stable corporate fundamentals. While isolated stress has emerged in certain sectors, default rates remain manageable and near long-term averages.

The senior-secured structure of floating-rate loans provides priority in the capital stack, offering an additional layer of protection in uncertain environments. For investors seeking income with reduced interest-rate sensitivity, this asset class remains a useful portfolio component.

High-Yield and Private Credit: Selectivity is Essential

Credit markets enter 2026 from a position of stability, but valuations warrant caution. Longer-term high-yield spreads remain below long-term averages, offering less compensation for credit risk than in prior cycles.

We are more constructive on high-quality, short-duration, high-yield assets to provide a defensive income solution, targeting shorter maturities to minimize interest rate sensitivity. This conservative approach offers attractive yields while prioritizing capital preservation and reducing default risk relative to the broader high-yield market.

Private credit remains a strategic allocation for portfolios seeking consistent income and diversification. Our view is balanced, as structural growth and rebounding M&A activity counteract cyclical pressures, while the asset class continues to face increased scrutiny of underwriting quality.

Declining interest rates are moderating yields on private loans, but the asset class maintains a steady premium over public markets. We are monitoring whether these benefits are being offset by rising leverage and margin compression among mid-market borrowers.

Consequently, performance is expected to remain resilient, though success depends heavily on disciplined credit selection.

TIPS: A Hedge Against Inflation Surprises

Treasury Inflation-Protected Securities (TIPS) continue to play an important role in managing inflation risk. Should inflation remain elevated or reaccelerate unexpectedly, TIPS provide explicit protection that traditional nominal bonds do not.

Fixed Income Perspective

While interest rates may continue to trend lower, fixed income remains materially more attractive than it was for much of the past decade. In our view, a balanced approach—emphasizing income, diversification, and risk management—offers the most effective way to navigate uncertainty and support broader portfolio objectives in 2026.

Alternatives Outlook: Diversifying Toward Durable Growth

In 2026, infrastructure appears poised to deliver durable returns, driven by AI and electrification demand. Simultaneously, real estate continues its gradual recovery as rates normalize. High-quality data centers and senior housing should outperform, bolstered by constrained supply and improved transaction flows. Together, these sectors offer resilient, inflation-linked growth fueled by strong secular tailwinds.

Commercial Real Estate: A Recovery Gaining Steam

We believe the commercial real estate market has transitioned from a period of a “valuation reset” to a recovery phase after the 2022-2023 selloff. With values hovering just above their recent low point following a challenging 2022–2024 period, we believe real estate offers compelling relative value compared with historically elevated valuations in equity and fixed-income markets.

The shifting macro environment, marked by declining interest rates and robust liquidity in the debt market, has transformed former headwinds into significant tailwinds. While traditional sectors such as residential and logistics remain resilient, digital infrastructure has been the clear outperforming subsector given the excitement around AI.

As large data center owners and investors (i.e., “hyperscalers”) pour trillions of capital into supporting the AI revolution, data centers have emerged as essential “picks and shovels” assets. In our view, this combination of historically low supply and the AI-driven “megatrend” creates one of the most attractive investment vintages in decades. Further, we believe supply/demand dynamics in multi-family and industrial warehouses also present an opportunity for owners over the next 3-5 years.

Infrastructure: Investing in What is Needed

Our outlook for infrastructure remains optimistic, underpinned by a historic surge in demand for power and digital connectivity. We believe the asset class has entered a structural growth phase as the global economy races to modernize aging grids, enhance supply chain resilience through onshoring, and execute on critical decarbonization goals. Many governments worldwide are already running large deficits and need private capital to fund infrastructure initiatives.

For example, regulated utilities and GDP-linked assets such as airports and toll roads are uniquely positioned to provide earnings stability. These assets typically operate under long-term contracts and favorable regulatory frameworks that shield them from broader market volatility.

We believe “preferred” assets (regulated utilities, toll roads, airports) benefit from contractual or regulated mechanisms that help offset inflation, alongside resilient, inelastic demand, which can support cash flows even if inflation moderates and rates remain elevated. Meanwhile, long-term infrastructure spending remains robust.

Equity Outlook: Mindful of AI Excitement

We enter 2026 constructive on equities, but increasingly mindful of valuation, concentration, and shifting leadership. While innovation—particularly in artificial intelligence—continues to drive earnings growth, the market environment is evolving in ways that reward selectivity and diversification over narrow exposure.

Rather than making a directional market call, our focus is on how opportunity differs across regions, sectors, and market capitalizations.

U.S. Large Cap Equities: Earnings Still Matter More Than Multiples

U.S. equities remain supported by resilient earnings, strong balance sheets, and a policy backdrop that is becoming more accommodative. However, valuations are elevated relative to historical levels, placing greater emphasis on earnings delivery rather than on further multiple expansion.

The S&P 500 enters 2026 trading near 22x forward earnings, above long-term averages. While this level does not imply an imminent market peak, it suggests that future returns will be driven more by earnings growth than by rising valuations—particularly in the most crowded market segments.

As interest rates decline, we expect leadership to continue broadening beyond the largest technology companies. This favors companies with durable cash flows, pricing power, and exposure to domestic investment trends tied to fiscal policy and infrastructure spending.

U.S. Mid- and Small-Cap Equities: Positioned for Broadening Leadership

Mid- and small-cap equities remain sensitive to financial conditions, making them natural beneficiaries of easing monetary policy. Entering 2026, lower borrowing costs, improving credit availability, and targeted fiscal incentives may provide a more supportive backdrop than in recent years.

Earnings growth expectations for smaller companies exceed those of large-cap peers, reflecting operating leverage to domestic growth and capital investment. While volatility is likely to remain higher than in large caps, periods of broadening market leadership have historically favored this segment following extended large-cap dominance.

International Equities: Policy Support and Valuation Opportunity

International equities outperformed in 2025, and we believe they can remain an important component of equity portfolios entering 2026. Compared with U.S. markets, international equities offer two advantages: less concentration and different economic and policy drivers.

Germany’s fiscal initiatives, along with broader European Union investment programs, are aimed at strengthening economic resilience. Combined with more attractive valuations and less market concentration than in the U.S., these factors improve the region’s relative appeal—particularly if global growth stabilizes.

Japan: Better fundamentals, but valuations are less forgiving

Japan continues to benefit from improving corporate governance, rising wages, and shareholder-friendly reforms. Buybacks and capital discipline remain supportive, and domestic economic momentum has improved.

That said, valuations have moved toward the upper end of historical ranges following strong performance. As a result, continued progress will depend more heavily on earnings growth and execution than on multiple expansion.

Emerging markets: Valuation support and earnings potential

Emerging-market equities enter 2026 with a meaningful valuation advantage over developed markets. Trading near 13x forward earnings and 18% earnings-per-share growth, the asset class offers a higher earnings yield and greater sensitivity to global growth.

- China: Equity performance has become increasingly disconnected from traditional measures of economic growth, reflecting the index’s heavier weighting toward technology and innovation-oriented companies. Policy support and AI-related investment may help sustain earnings, even as broader economic challenges persist.

- EM ex-China: Earnings growth expectations remain strong, supported by technology leaders in Asia and improving financial conditions in countries such as India.

What the Equity Outlook Means for Investors

The equity opportunity set in 2026 is less about market direction and more about composition. Elevated valuations in select areas coexist with more attractively priced opportunities elsewhere, particularly where policy support, earnings growth, and valuation discipline intersect.

For investors, this reinforces the importance of diversification across regions and market capitalizations. Participating in innovation remains important, but doing so with valuation awareness and balance is essential.

Equity Perspective

We remain cautiously optimistic on global equities entering 2026. While volatility is likely to persist as leadership continues to evolve, the combination of earnings growth, easing financial conditions, and supportive policy creates a constructive but selective environment.

In our view, disciplined diversification remains the most effective way to capture opportunity while managing risk in a rapidly changing market landscape.

Concluding Thoughts

As we enter 2026, the investment landscape reflects a period of transition rather than disruption. The forces shaping markets—technological change, evolving policy dynamics, and shifting sentiment—do not point to a single, predictable outcome. Instead, they reinforce the importance of thoughtful portfolio construction, selectivity, and discipline.

The experience of the past year underscores this perspective. While markets delivered strong results, leadership was concentrated, policy expectations evolved, and sentiment remained cautious. These dynamics shaped today’s opportunity set and inform how portfolios are positioned going forward.

Looking ahead, opportunities exist across asset classes and regions, particularly where earnings growth, policy support, and valuation discipline intersect. At the same time, risks remain, and market cycles rarely move in straight lines. For this reason, our focus remains on diversification, risk management, and long-term objectives rather than short-term market forecasts.

While past performance does not guarantee future results, we believe that a disciplined investment approach, grounded in diversification, periodic rebalancing, and an understanding of evolving market dynamics, provides the most reliable foundation for navigating uncertainty and pursuing long-term financial goals.

As always, portfolios are constructed with each client’s unique circumstances in mind. Our role is not to predict markets, but to steward capital thoughtfully through changing environments, remaining focused on resilience, opportunity, and long-term success.

Previous Posts

- Sage Insights: Fed Policy Turning Point, AI Enters a New Phase

- Sage Insights: Market Resilience Despite Short-Term Uncertainty

- Sage Named Among Top Financial Advisory Firms

Learn More About Sage

Disclosures

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks, or estimates in this letter are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks, or assumptions should not be construed to be indicative of the actual events that will occur. These projections, market outlooks, or estimates are subject to change without notice. Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, product, or any non-investment-related content referred to directly or indirectly in this newsletter will be profitable, equal to any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer reflect current opinions or positions. All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual client portfolio returns may vary due to the timing of portfolio inception and/or client-imposed restrictions or guidelines. Actual client portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in managing an advisory account. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Sage Financial Group. To the extent that a reader has any questions regarding the applicability above to his/her situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. Sage Financial Group is neither a law firm nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of Sage Financial Group’s written disclosure statement discussing our advisory services and fees is available for review upon request. Copyright 2026.