Although February is the shortest month of the year, it was no less eventful as market participants digested corporate earnings, economic data, and the new administration’s trade-related announcements.

In this edition of Insights, we examine key developments, including the impact of tariff announcements, fluctuations in the Treasury market, and the dispersion of stock performance leaders following the latest earnings season.

As we head into March, our focus remains on helping our clients position their portfolios to navigate various scenarios in the global economy and markets. We believe diversification across asset classes, geographies, and investment strategies is the most sensible strategy for accomplishing their investment goals.

Market Performance: The Case for Diversification

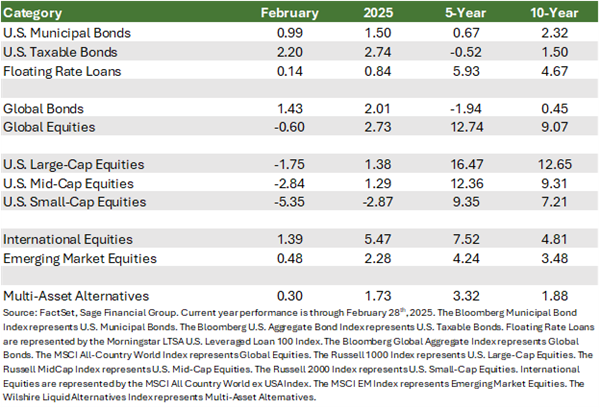

February underscored the importance of diversification. Five of the seven largest U.S. companies by market capitalization declined during the month as investors grappled with concerns about inflation and growth. It is notable, however, that Sage’s equity positions performed with considerably less volatility. Conversely, fixed-income, international equities, and alternative investments delivered positive returns, reinforcing the value of a well-balanced portfolio.

Global Fixed Income returned a strong 1.43% in February, as falling yields and geopolitical uncertainty around tariff implementation provided a tailwind for bond investors.

- U.S. Taxable Bonds: Investment-grade fixed income rose 2.20%, as longer-term bond yields fell in the second half of the month in response to investor concerns over the impact tariffs could have on growth.

- U.S. Tax-Exempt Bonds: Increased by 0.99%, supported by ongoing investor demand for tax-advantaged assets.

- Floating Rate Loans: Delivered a modest 14% return, as widening credit spreads created a slight headwind. We continue to favor these assets, given the expectation that short-term rates will remain elevated for longer.

Global equities saw mixed performance, declining by 0.60% overall. U.S. and international stocks moved in opposite directions, the former declining and the latter gaining. While U.S. equities represent more than two-thirds of the global equity market, exposure to European and emerging markets cushioned investors during a period of domestic selling, further underscoring the importance of geographic diversification within investment portfolios.

- U.S. Large-Cap Equities: Retreated by 1.75%, despite over 75% of companies exceeding earnings forecasts. U.S. large-cap stock valuations remain above historical averages, creating elevated expectations. Stock prices of companies that missed earnings experienced an outsized decline.

- U.S. Mid- and Small-Cap Equities: Fell 2.84% and 5.35%, respectively, in February. Stronger-than-anticipated inflation data reduced the probability of near-term rate cuts from the Fed, and the pressure of higher rates weighed on smaller companies’ balance sheets, as they tend to carry more debt than larger companies. At the same time, investors lowered their expectations that the new administration’s policies would positively influence domestic companies.

- International Equities: Provided stability, with international large-cap stocks returning 39%, supported by strong corporate earnings and the fact that inflation remains on target for the European Central Bank. Emerging market equities delivered a positive return of 0.48%, as investors responded favorably to China’s advancement within AI and a rare meeting between China’s President Xi Jinping and the founders of publicly traded Chinese tech companies.

Trade Policy Reverberations

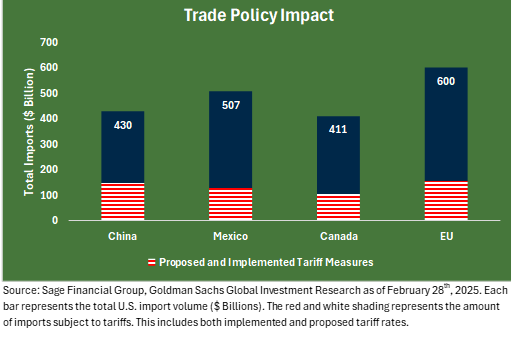

Tariffs remain at the forefront of the daily news cycle and have led to uncertainty for investors around what these new trade policies could mean for economic growth and inflation. Recent actions include:

- A 10% tariff increase on $430 billion of Chinese imports began on February 4th, and an additional 10% tariff on imported Chinese goods is set to take effect in early March.

- Proposed 25% tariffs on goods from regional trading partners in Mexico and Canada have been delayed, and their implementation is expected on March 4th.

- The discussion of 25% tariffs on European auto and broader imports, which would impact the largest U.S. trading partner measured by import volume.

The graphic below illustrates the volume of imports the U.S. receives from these trading partners. Each bar represents the amount of imported goods from each country/economic union. The red and blue lines capture the expected number of goods expected to be placed under a new tariff rate.

If fully implemented, the total volume of goods impacted would total more than $530 billion. Markets are particularly susceptible to the inflationary risks of these policies. Companies with pricing power can pass costs along to consumers, potentially driving inflation higher and keeping Fed rate cuts on hold to avoid an overheated economy. Additionally, there is a risk that consumers and businesses may delay spending plans while this economic volatility gets sorted out.

Using history as a guide, including the 2018 trade conflicts, the impact of trade policy tends to be short-lived. Markets will likely continue to react to underlying developments and headlines in anticipation of future policies. But as we always say, time in the market beats timing the market. Our goal is to construct portfolios that meet our clients’ financial goals across a variety of economic and market conditions.

We believe the best defense against volatility is a portfolio well-diversified across asset classes and geographies. This type of portfolio remains a prudent way to mitigate risks and capture opportunities. When appropriate, Sage recommends investments like floating rate loans, short-duration high yield, and infrastructure, which we expect to perform consistently across a variety of market environments. We encourage you to keep the recent volatility in perspective, given the strong performance we have experienced over the past 1, 3, 5, and 10+ years.

Cues from the Bond Market

Longer-term Treasury yields declined by 0.36%, as the 10-year yield fell from 4.55% to 4.19%. This decline provided a tailwind for bonds and led the Bloomberg U.S. Aggregate Index to its strongest performance since July 2024.

The drop in yields suggests investors anticipate slower economic growth rather than falling inflation. While inflation expectations remain stable, recent policy signals contributed to bond market movement. Notably, newly confirmed Treasury Secretary Scott Bessent outlined his plans to lower Treasury yields while preserving Federal Reserve independence. Alongside the recent tariff announcements, these plans added another layer of complexity to the economic outlook.

Dispersion of Market Leadership Among Equities

U.S. equities had a muted start to the year, following a decade of U.S. exceptionalism dominated by large-cap tech stocks. While we remain cautiously optimistic about U.S. equities, we expect earnings growth and valuations to provide a catalyst for future international equity returns.

So far in 2025:

- The Magnificent Seven[1] stocks have fallen nearly 6.0%

- The average U.S. large-cap stock[2] has gained 2.9%.

This dispersion highlights opportunities beyond the most concentrated names in the S&P 500. Key areas for investors to watch include:

- Emerging Markets: Positive transformations in artificial intelligence (AI) are impacting stocks across the globe as emerging market stocks rose 0.5% in February. Chinese companies are announcing further investments following the release of DeepSeek, and consumer-focused names across Asia and South America report strong corporate earnings.

- European Markets: A pro-market election outcome in Germany and manufacturing growth are positive developments, as European stocks most recently increasing by 3.7% in February.

A slowing U.S. economy may present opportunities for stocks abroad. As inflation returns to target levels, several major central banks—including the Bank of England and the European Central Bank—are expected to implement stimulative measures by reducing borrowing, supporting international equity markets, and driving strong earnings growth in 2025.

Implications for Your Portfolio

Despite ongoing volatility, markets have begun the year on solid footing. While we expect volatility to persist, we are cautiously optimistic about the economy broadly, and our investment approach remains anchored in economic fundamentals.

- Fixed Income: Stickier-than-anticipated inflation has delayed Fed rate cuts. To balance against bond market volatility, we selectively leverage less interest-rate sensitive strategies such as bank loans and high-yield markets while maintaining core bonds for diversification should rates continue to fall because of lower growth expectations.

- Alternatives: Real estate and private equity stand to benefit from deregulation and lower interest rates (i.e., a falling 10-year yield is good for these assets). Infrastructure investments should also perform well in an inflationary environment. Selective exposure to these asset classes can increase portfolio diversification and improve expected returns.

- Equities: The impact of higher rates on U.S. small- and mid-cap stocks should wane over time. To diversify exposure away from the U.S., developed market equities are experiencing better-than-expected earnings growth, supported by ongoing stimulus from the European Central Bank and others. A conclusion to the war in Ukraine should benefit global risk sentiment.

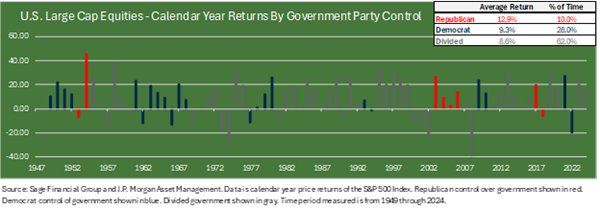

It is also worth a reminder that historically, as shown in the graph below, market returns do not significantly differ by government control.

Closing Thoughts

We maintain a cautiously optimistic outlook on the economy and the markets.

We are continuing to intently scrutinize incoming data to discern any indications of a potential shift in business activity–particularly shifts stemming from tariff-related announcements, fluctuations in the Treasury market, and the dispersion of stock performance following the latest earnings season. These factors are critical in understanding whether we are observing slight changes or a more significant inflection point in the current business cycle.

Markets may continue to experience volatility, which is normal behavior, but we believe long-term success is rooted in disciplined investing and diversification. Our carefully constructed portfolios are designed to weather market fluctuations while keeping each client’s time horizon and unique financial goals in focus.

As always, we are here to help guide you through these dynamics.

Footnotes

[1] Apple, Microsoft, Nvidia, Google, Amazon, Meta, and Tesla

[2] Measured by the S&P 500 Equal-Weighted Index.

Previous Posts

- Sage Insights: Navigating Markets in the New Year

- Sage 2024 Performance Review and 2025 Investment Outlook: Positioning for Opportunity in a Changing Landscape

- Sage Insights: Navigating Markets After the Election

- Our Perspective: On the 2024 U.S. Elections

-

Learn More About Sage

Disclosures

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks, or estimates in this letter are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks, or assumptions should not be construed to be indicative of the actual events that will occur. These projections, market outlooks, or estimates are subject to change without notice. Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, product, or any non-investment-related content referred to directly or indirectly in this newsletter will be profitable, equal to any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer reflect current opinions or positions. All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual client portfolio returns may vary due to the timing of portfolio inception and/or client-imposed restrictions or guidelines. Actual client portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in managing an advisory account. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Sage Financial Group. To the extent that a reader has any questions regarding the applicability above to his/her situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. Sage Financial Group is neither a law firm nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of Sage Financial Group’s written disclosure statement discussing our advisory services and fees is available for review upon request.