2025 began with no shortage of market-moving events, as the change in the White House brought uncertainty about how different leadership and economic policies could impact global markets. In this edition of Insights, we examine key recent developments, including the emergence of tariff-linked policies, the Federal Reserve’s decision to pause rate cuts, and competition among key players in artificial intelligence (AI).

As we move into another month, our priority remains to prepare our clients’ investment portfolios for a wide range of outcomes amidst this fast-changing market cycle by diversifying across asset classes, geographies, and strategies.

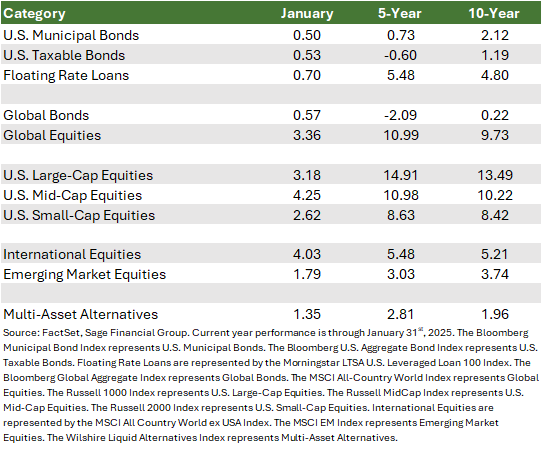

Market Performance: A Favorable Start to the New Year

Financial markets kicked off 2025 on a positive note, though not without some volatility. Investors digested critical inflation data and continuous geopolitical announcements, but overall, major asset classes posted gains.

Global fixed income gained 0.57% in January, as economic growth slowed more than anticipated in the fourth quarter, leading to falling yields and supportive ongoing central bank easing.

- U.S. Taxable Bonds: Investment-grade fixed income rose 0.53%. Key inflation indicators pointed toward a gradual decline, prompting interest rates to reverse course mid-month and end January slightly lower than in December 2024.

- U.S. Tax-Exempt Bonds: Increased by 0.50%, supported by investor demand for tax-advantaged assets amid heightened bond issuance.

- Floating Rate Loans: Rose 0.70%, as corporate fundamentals remained strong and short-term yields stayed elevated.

Global equities climbed 3.36%, with U.S. and international markets participating in the rally. A key tailwind for non-U.S. stocks was a modestly weaker dollar, which helped level the playing field for international stocks.

- U.S. Large-Cap Equities: Increased by 3.18%, driven by positive earnings. Roughly one-third of U.S. large caps reported earnings, while positive surprises were widespread. This contributed to the average stock outperforming the market-cap weighted index by 0.72% during the month.

- U.S. Mid- and Small-Cap Equities: Mid-caps were the standout performers, gaining 4.25%, while small-caps recorded an admirable 2.62% gain. Optimism was tied to expectations that the new administration’s policies would favor smaller industrial manufacturers and banks.

- International Equities: As measured by the most widely referenced index, international large-cap stocks returned a solid 4.03%, boosted by European Central Bank rate cuts and Japan’s export-facing economy benefitting from currency weakness. Emerging market equities rose a more moderate 1.79% as investors continued to digest the fluctuating news over tariffs and trade policy.

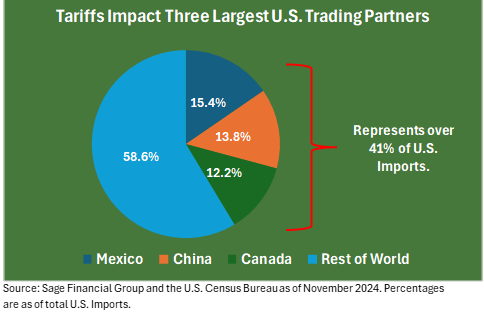

Trump’s Agenda: Trade Policy in Focus

As we wrote in our 2025 Investment Outlook: Positioning for Opportunity in a Changing Landscape, Trump’s return has “ushered in a new era of economic policy, marked by deregulation, tax reform, and trade adjustments.” While deregulation and tax reform are generally market-friendly, trade policy adjustments present risks that we are witnessing in real time.

In late January, the White House team announced new tariffs, which can be thought of as a toll fee for bringing goods across borders:

- 25% duties on Mexican and Canadian imports (with 10% on Canadian energy)

- 10% tariffs on all Chinese imports

The White House is positioning these measures as a response to the manufacturing and export of illicit fentanyl and border security concerns. All three of the tariffed countries have pledged to respond.

- Canada proposed and then backed off of retaliatory 25% tariffs on a wide range of U.S. exports after announcing a reprieve and a plan for border reinforcement.[1]

- China vowed “corresponding countermeasures” and intends to appeal to the World Trade Organization (WTO). [2]

- Mexico negotiated a reprieve by deploying 10,000 troops to the Mexican border to combat drug trafficking.[3]

Equity markets initially responded negatively to the broad nature of the tariffs and the subsequent responses by each of the governments, which are the three largest trading partners of the U.S., given that the moves could raise the cost of food, autos, and consumer goods in the near term and slow economic growth. Bonds, however, performed well initially, demonstrating the power of diversification.

In our view, we are still in the early innings of these trade conflicts, and it is too soon to know the totality and duration of these tensions, particularly given the complexity of global markets.

For example, in the auto sector, GM and Ford are U.S. companies, but many of their cars are made in Mexico. Tesla exports a significant volume to Canada. Individual components that are used to manufacture vehicles may cross both the U.S./Canada and U.S./Mexico border multiple times.

As these trade disputes evolve, we maintain that a diversified portfolio approach is a prudent way to mitigate risks and capture opportunities.

Federal Reserve: A Pause in Rate Cuts

At its first meeting of 2025, the Federal Open Market Committee (FOMC) elected to hold interest rates steady. This marked a shift following three consecutive meetings where interest rates were cut.

FOMC Chairman Powell noted that interest rates remain in “restrictive territory,” meaning they are high enough to slow economic growth in a way that supports the FOMC’s dual mandate of full employment and price stability.

The Fed’s decision to pause was grounded in:

- Resilient economic growth

- A strong labor market

- Gradual progress on inflation

From an investor’s perspective, a Fed rate pause signals stability for bond markets, helping to keep longer-term bond yields range-bound. This benefits borrowing costs, corporate debt issuance, and M&A activity. Lower rates historically provide tailwinds for equities and alternative assets such as real estate and private equity.

DeepSeek Chatter: A Disruptive Shift in AI

The AI landscape saw a potential paradigm shift with the rise of DeepSeek, a startup funded by the Chinese hedge fund High-Flyer. In November 2024, DeepSeek previewed its latest large language model, claiming capabilities comparable to OpenAI’s most advanced model, o1, despite dramatically lower training costs.

The implications are significant:

- DeepSeek claimed to have spent only $5.6 million on training, compared to the hundreds of millions spent by big tech companies like Amazon, Microsoft, Meta, and Alphabet.

- AI hardware spending could decline, disrupting expectations that films that billions, if not trillions, would need to be spent on purchasing graphic processing units (GPUs) from companies like Nvidia.

- Stock market impact: The initial market reaction was mixed. For example, leading chip maker Nvidia saw its value collapse by $554 billion in just one week, while other companies saw a rise in market values as they may need to spend less on chips.

While fully independent verification of DeepSeek’s claims about matching OpenAI’s capabilities has been challenging due to the lack of standardized testing methods, some U.S. AI specialists have been impressed. An important risk we noted in our 2025 Outlook is that companies have invested heavily in the growth of AI, and expectations are high. The ability to deliver remains paramount.

In our view, the ability to reduce building and training costs could accelerate AI adoptions and broadly benefit technology stocks and economic productivity. Greater efficiency in capital expenditures by Amazon and the other large technology companies should mean that this revolutionary technology spreads across industries more quickly.

Implications for Investment Portfolios

After a strong 2024, we know complacency can become a weakness. We remain focused on consistently monitoring market-moving forces and their potential to impact our clients’ investment portfolios. This includes the new administration’s policies, the health of corporate America, and monetary policy expectations.

- Fixed Income: Risks of upward pressure on inflation may create potential challenges for core bonds. However, higher yields offer a better starting point for bond investors than in 2022. Corporate credit exposure remains attractive, given strong U.S. earnings trends. International bonds stand to benefit from ongoing central bank easing in Europe. The extent of easing will depend on the strength of the Euro relative to the dollar.

- Alternatives: Real estate and private equity stand to benefit from deregulation and stable interest rates. Inflation remaining elevated should benefit infrastructure as companies with pricing power can push through costs. Selective exposure to these asset classes offers the potential to increase portfolio diversification and improve expected returns.

- Equities: U.S. small- and mid-cap stocks continue to be the most attractive in our view due to their exposure to domestic economic growth. Developed market equities remain dependent on earnings growth and the propensity of the ECB to stimulate growth in Europe. Emerging market equities are likely to remain challenged by ongoing trade tensions between the U.S. and China.

Closing Thoughts

In our view, the economic outlook remains cautiously constructive. The new administration’s policies, especially those related to trade and immigration, will shape market conditions in the coming months. While the near-term economic environment appears stable, unexpected developments could shift market sentiment quickly.

We encourage our clients to stay disciplined and committed to their personalized investment plans.

Footnotes

[1] https://www.nbcnews.com/politics/economics/mexicos-president-says-tariffs-will-delayed-one-month-rcna190433

[2] https://www.bloomberg.com/news/articles/2025-02-02/xi-weighs-retaliation-after-trump-hits-china-with-10-tariff

[3] https://www.cnbc.com/2025/02/03/trump-tariffs-mexico-canada-china-sheinbaum-responds.html

Previous Posts

- Sage 2024 Performance Review and 2025 Investment Outlook: Positioning for Opportunity in a Changing Landscape

- Sage Insights: Navigating Markets After the Election

- Our Perspective: On the 2024 U.S. Elections

- Sage Insights: Market Resilience Amidst Volatility

-

Learn More About Sage

Disclosures

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks, or estimates in this letter are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks, or assumptions should not be construed to be indicative of the actual events that will occur. These projections, market outlooks, or estimates are subject to change without notice. Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, product, or any non-investment-related content referred to directly or indirectly in this newsletter will be profitable, equal to any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer reflect current opinions or positions. All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual client portfolio returns may vary due to the timing of portfolio inception and/or client-imposed restrictions or guidelines. Actual client portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in managing an advisory account. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Sage Financial Group. To the extent that a reader has any questions regarding the applicability above to his/her situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. Sage Financial Group is neither a law firm nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of Sage Financial Group’s written disclosure statement discussing our advisory services and fees is available for review upon request.