The first half of 2025 delivered its share of twists and turns—marked by bouts of volatility, periods of resilience, and a strong recovery. Investors navigated a challenging mix of geopolitical tensions, persistent inflation concerns, and a notable shift in market leadership.

Following a sharp early spring decline driven by proposed tariffs, a powerful relief rally extended through June, propelling U.S. stocks to all-time highs as trade tensions eased and the domestic economy continued to demonstrate strength. A healthy labor market and steady consumer spending have so far defied recession fears, helping sustain investor confidence.

In this edition of Insights, we explore three key themes shaping today’s investment landscape:

- A resilient economy supporting markets through geopolitical uncertainty.

- A surge to all-time highs for U.S. equity indices.

- The continued evolution of generative Artificial Intelligence and its potential long-term impact.

Resilient Markets Climb

June brought positive returns across all major asset classes, reflecting improved sentiment and a renewed sense of optimism among investors.

Fixed Income Markets

- Global bonds rose 1.9% in June, with investment-grade corporate credit leading the way.

- U.S. taxable bonds gained 1.5% as interest rates dropped in June after the Consumer Price Index showed slowing inflation.

- U.S. tax-exempt bonds increased 0.7%, buoyed by nine consecutive weeks of steady demand following tax season.

- Floating-rate loans added 0.6%, supported by the Federal Reserve’s measured approach to policy changes in 2025.

- International bonds climbed 2.2%, helped by a European Central Bank rate cut earlier in the month and relative currency stability in Japan and the UK.

Equity Markets

- Global equities returned 4.5% in June, lifted by easing trade tensions and resilient corporate earnings.

- U.S. large-cap equities led with a 5.1% gain, driven by a strong jobs report and continued growth in corporate earnings.

- U.S. mid- and small-cap equities rose 3.7% and 5.4% during the month, supported by an increase in mergers and acquisitions (M&A) activity. Small-cap stocks can be acquisition targets for larger companies.

- International equities remain ahead of U.S. stocks in 2025 and concluded the month by rising 3.4%, as European fiscal measures boosted investor confidence.

- Emerging market equities posted a substantial 6.0% gain, helped by Chinese stimulus efforts and India’s relative insulation from tariff impacts.

Year-to-date, international equities and emerging market equities have led the markets, up 17.9% and 15.3%, respectively. For investors, this broad-based strength highlights the benefits of a diversified portfolio—one designed to participate in growth while helping cushion against uncertainty.

Markets Absorb Geopolitical Shocks and Push Forward

War is inherently tragic, and its sadness is most acutely felt in the profound and irreversible loss of human life. In mid-June, the conflict between Israel and Iran escalated into direct military confrontation, underscoring how quickly geopolitical risks can spill over into financial markets.

Oil prices initially surged as investors feared that Iran, a major oil producer, could disrupt supply through the Strait of Hormuz, a critical chokepoint for approximately 20% of the world’s oil supply. A prolonged disruption would have posed two key challenges:

- Inflationary Pressure: Higher oil prices could have increased production costs across many industries, potentially leading to higher inflation and affecting consumers.

- Central Bank Dilemma: Rising energy costs might limit the flexibility of central banks, particularly those already in a rate-cutting cycle, by forcing policymakers to reconsider their plans.

As the situation showed signs of containment and a ceasefire was reached, oil prices reversed sharply, ending the month little changed. Stock markets stabilized and, in some cases, regained earlier losses.

Episodes like this serve as an essential reminder: while geopolitical events can create temporary volatility, history shows that markets tend to refocus on long-term fundamentals—economic growth, innovation, and inflation trends.

A more stable environment often brings renewed confidence, encouraging investors who temporarily moved into safe-haven assets to return to equities and higher-yielding bonds. This shift from caution back to risk-taking can help support broader market recoveries over time.

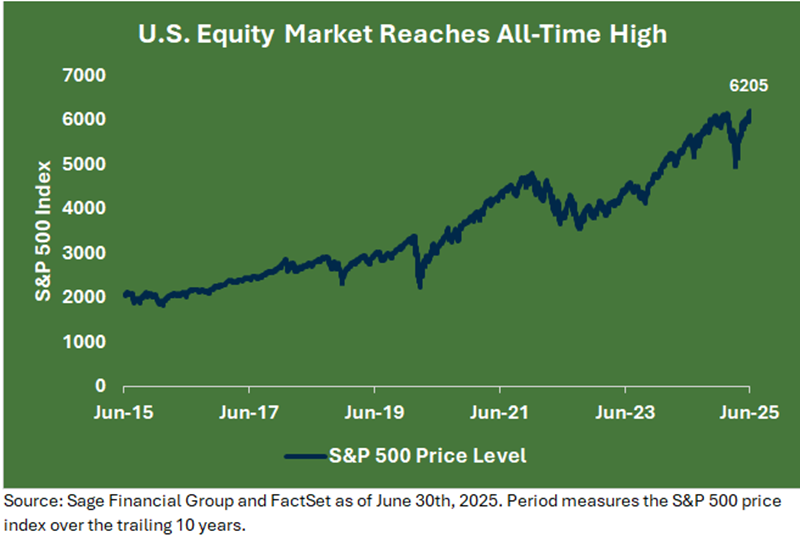

New Highs – and the Value of Staying Invested

Despite persistent headlines about tariffs and inflation, U.S. large-cap stocks reached all-time highs in late June. Just weeks earlier, the S&P 500 had dipped below 5000, before rebounding nearly 25%.

This pattern highlights a key truth: some of the strongest market gains often occur during or just after periods of extreme stress. While the idea of buying at the absolute bottom and selling at the absolute top is alluring, history consistently shows that staying invested through volatility is more effective in supporting long-term goals for most investors.

At Sage, we do not try to predict every twist and turn in the market. Instead, we focus on helping our clients build a diversified portfolio designed to weather a wide range of scenarios, with the objective of keeping their plan on track.

Generative AI: The Long Arc of Transformation

Generative AI is ushering in a new era of technological advancement and operational excellence that has been the backbone of markets over the last two years.

We see four phases of adoption underway:

- Hardware: Companies like NVIDIA (NVDA) are building the advanced chips essential to AI development.

- Infrastructure: Platforms like Amazon Web Services and Microsoft Azure enable AI applications to operate at scale through their cloud capabilities.

- Platform: Emerging applications are enhancing user experiences and streamlining workflows.

- Efficiencies: The widespread adoption of AI technologies will help businesses boost productivity and drive higher profit margins.

We believe the transformation is fundamental and may provide favorable tailwinds for various industries, business models, and the economic landscape. As companies move deeper into the platform and efficiency phases, productivity across the entire economy may be boosted, similar to other inventions such as the steel plow, factory electrification, and the internet. Higher productivity and economic growth could support strong returns in stocks and bonds through earnings growth, along with less inflationary pressure.

At the same time, it is natural for expectations to outpace reality occasionally. Our approach aims for portfolios to participate in innovation while maintaining balance and avoiding overconcentration in any single theme.

Closing Thoughts

Markets will always experience cycles of optimism and concern. But it is through these periods that patience, discipline, and perspective prove their worth. Staying focused on your goals, time horizon, and risk tolerance—and on the strategy built to align with them—can bring clarity and peace of mind when headlines are uncertain.

Learn More About Sage

Disclosures

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks, or estimates in this letter are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks, or assumptions should not be construed to be indicative of the actual events that will occur. These projections, market outlooks, or estimates are subject to change without notice. Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, product, or any non-investment-related content referred to directly or indirectly in this newsletter will be profitable, equal to any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer reflect current opinions or positions. All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual client portfolio returns may vary due to the timing of portfolio inception and/or client-imposed restrictions or guidelines. Actual client portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in managing an advisory account. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Sage Financial Group. To the extent that a reader has any questions regarding the applicability above to his/her situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. Sage Financial Group is neither a law firm nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of Sage Financial Group’s written disclosure statement discussing our advisory services and fees is available for review upon request.