September is historically one of the weaker months for markets, yet this year it defied that pattern. Stocks pushed higher and bond prices rose after the Federal Reserve delivered its first rate cut in nine months. In this edition of Insights, we highlight three themes that shaped the month:

- Trade policy remains a risk, but its economic impact to date has been less severe than expected.

- The Federal Reserve’s “risk-management cut” on September 17 signaled a proactive effort to support growth.

- Mergers and acquisitions surpassed $800 billion this year, as traditional software firms aggressively acquired Artificial Intelligence (AI) startups, providing a tailwind for outperforming technology stocks.

Meanwhile, the U.S. federal government officially shut down on October 1, after Congress failed to pass necessary funding legislation amid partisan disagreement over key issues. While shutdowns can be disruptive in the short term, financial markets have historically viewed them as temporary, with their impact limited.

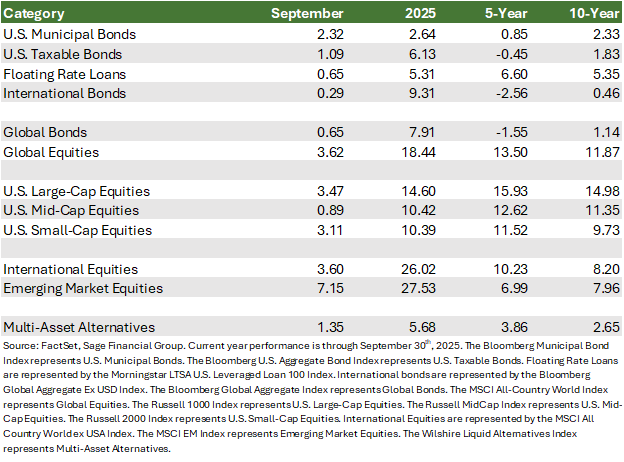

Monthly Market Wrap

Evolving monetary policy and economic narratives influenced market trends in September. Fixed income markets generally saw modest gains, while equity markets advanced broadly.

Fixed Income Markets

- Global Bonds rose 0.7%, as U.S. policymakers began to ease rates lower, while most international central banks held steady.

- U.S. Taxable Bonds gained 1.1%, as rates declined, though strong economic growth and sticky inflation tempered investor enthusiasm.

- U.S. Tax-Exempt Bonds increased by 2.3%, supported by slowing municipal bond issuance and falling rates.

- Floating-Rate Loans added 0.7%, continuing to benefit from investor interest in their elevated income potential.

- International Bonds marginally rose 0.3% after initial volatility in the Japanese and European markets, before government yields settled at the end of the month.

Equity Markets

- Global Equities advanced 3.6%, as the U.S. economy continues to expand, easing fears of a worldwide slowdown.

- U.S. Large-Cap Equities continued to deliver, rising 3.5%, supported by sustained growth in the artificial intelligence sector.

- U.S. Mid-Cap Equities modestly rose 0.9%, because they are seen as less directly supported by AI enthusiasm or rate cut momentum.

- U.S. Small-Cap Equities gained 3.1% after briefly reaching all-time highs toward the middle of the month, lifted by stronger growth forecasts.

- International Equities also rose 3.6% as a détente in trade tensions allowed investors to focus on positive quarterly earnings.

- Emerging Market Equities rallied 7.2%, led by China’s support for its tech industry and the continuing acceleration of the Indian economy.

Tariffs: Economic Drag Proves Smaller Than Feared

The initial phase of U.S. tariffs created economic uncertainty and volatility in the financial markets earlier this year. Yet their impact on the economy has been less severe than feared.

- Constructive Negotiations: After peaking near 25% in April, the aggregate tariff rate settled at 15% as new trade deals were finalized.

- Corporate Strategies and Delayed Pricing: Companies have softened the near-term impact of the tariff increase by drawing down pre-tariff inventories, rerouting supply chains, and negotiating with suppliers. These measures have delayed the full effect of higher costs, but their benefit will diminish over time.

We continue to believe that tariff increases will remain a modest drag on the economy through the next couple of quarters before waning in 2026. Markets are treating them as manageable and one-time in nature, with equities discounting revenue effects.

For investors, we continue to recommend exposure to both domestic and international stocks as part of a diversified portfolio that can benefit from ongoing global economic growth.

At the same time, we view high-quality bonds as a stable and defensive component in the event that growth slows further.

Fed Ends Nine-Month Pause with Rate Cut

On September 17, the Federal Open Market Committee (FOMC) voted to lower the Fed Funds Rate by 0.25%, with the newest member, Stephen Miran, dissenting in favor of a deeper 0.50% cut. Chair Powell described the move as a “risk management cut,” noting that risks have shifted away from persistent inflation and toward a slowing labor market.

Several dynamics shaped this decision:

- Labor Market: Hiring has slowed meaningfully, even though layoffs remain low—a trend that may reflect structural shifts tied to technology and AI.

- Tariff Inflation: The inflationary effect of tariffs has been smaller and slower to materialize than initially feared, giving the Fed more flexibility.

- Data Volatility: Government data remains noisy, with frequent revisions expected to continue until survey response rates improve.

For investors, the implications are twofold. Lower rates reduce borrowing costs, which can support corporate profits and make equities more attractive relative to bonds. In fixed income, falling rates increase the value of existing longer-duration bonds, but they also mean new bonds will carry lower yields, tempering future return expectations.

Overall, a rate cut is an economic stimulus, and as September showed, it can lift both stocks and bonds. We believe that a diversified allocation across equities, fixed income, and real estate assets remains a prudent way to prepare for various outcomes, helping to smooth the investment journey while reducing reliance on any single driver of returns.

Mergers & Acquisitions Surge

U.S. mergers and acquisitions (M&A) are on track to increase by 40% this year, potentially surpassing $810 billion. AI is the primary driver:

- AI Startups: AI-related acquisitions have already exceeded the volume of the prior three years combined.

- Traditional Firms: Established software companies are buying AI startups at a record pace to integrate new capabilities and remain competitive.

- Consolidation: Some traditional software players are merging to achieve scale and efficiency.

If the rise in M&A activity can be sustained, we believe it generally reflects improving corporate confidence and easier access to capital, which can bolster economic growth.

For investors, this trend could benefit small-cap stocks (often acquisition targets), as well as private assets such as real estate and private equity. At the same time, frenzied M&A underscores the need for careful selection, favoring established companies over more speculative startups.

Closing Thoughts

September highlighted the crosscurrents shaping the markets: tariffs proving less damaging than feared, the Fed taking proactive steps to support growth, and AI-driven M&A fueling new opportunities.

At Sage, we view these developments as reminders of the importance of diversification. Our approach seeks to limit reliance on any single factor and keep portfolios aligned with what matters most – your goals, time horizon, liquidity needs, risk tolerance, and unique circumstances.

Learn More About Sage

Disclosures

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks, or estimates in this letter are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks, or assumptions should not be construed to be indicative of the actual events that will occur. These projections, market outlooks, or estimates are subject to change without notice. Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, product, or any non-investment-related content referred to directly or indirectly in this newsletter will be profitable, equal to any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer reflect current opinions or positions. All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual client portfolio returns may vary due to the timing of portfolio inception and/or client-imposed restrictions or guidelines. Actual client portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in managing an advisory account. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Sage Financial Group. To the extent that a reader has any questions regarding the applicability above to his/her situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. Sage Financial Group is neither a law firm nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of Sage Financial Group’s written disclosure statement discussing our advisory services and fees is available for review upon request.